PNN – Current trends, especially in the military and economic spheres, indicate a shift in the global situation from a state of “deterrent balance and equilibrium” to “pre-offensive operational readiness,” a pattern that will make some regions susceptible to conflict and confrontation between powers and a possibility of World War III.

A look at the current conditions in the world and the analyses that are included in the output of international think tanks indicate that the future situation could differ in many ways from the current conditions. In this context, examining the important military-security and economic components of the world outlines a traceable global pattern that is moving from a state of “deterrent balance and equilibrium” to “pre-offensive operational readiness.” A situation that, in the military sphere, has been manifested above all in the continuous increase in indicators such as troop mobility, the intensity of exercises, military communications, and strategic mobilization in most countries, including the United States, Russia, China, and Iran.

These trends have usually been accompanied by the development of cyber and information fields, each of which requires careful and meticulous examination separately. The economic field, if we look at it from a strategic perspective, has been the second pillar of these major developments over the past 18 months. Observation of available statistics and figures indicates that most countries have increased their defense budgets relative to GDP, and gold and foreign exchange reserves in the lands of the Eastern powers (China, Russia, and India) have also grown.

These changes come at a time when Western countries such as the United States and the United Kingdom, with high levels of public debt, have entered a stage of chronic financial vulnerability; a point that alone explains why Eastern countries, and China in particular, are accelerating their move to confront the West and achieve a greater share of the global economy.

The important point in this regard is that these developments are not merely tactical, but rather signal a significant and structural shift in the way geopolitical competition is faced; a long-term preparation for multi-front and hybrid conflicts, the signs of which are clearly visible. Although it is not possible to determine the exact time for entering the stage of all-out confrontation, the principle of confrontation cannot be denied.

A review of these conditions suggests that over the past eighteen months, several strategic trends have received more attention than others:

Growth of military indicators among world powers

Western and Eastern countries such as the United States, Russia, and China have seen growth in operational indicators including exercises, force mobility, cyber-readiness, strategic mobilization, and military communications.

A review of expert opinions and research studies shows that this coordination is not accidental and represents a global operational phase at the gray level, meaning multi-layered tactical readiness; an event that is completely unprecedented in the history of international relations, especially in the period before the First and Second World Wars.

A notable point in this regard is that the increase in the average military score of countries between 2024 and 2025 shows that many countries are not simply conducting exercises, but are actually installing infrastructure, secretly moving forces, strengthening command communications, and preparing for multi-front scenarios.

Shifting strategic weight towards militarism in the East and chronic financial pressure in the West

A review of the statistics and figures available over the past eighteen months shows that China and Russia are replacing Western balance with “economic deterrence” by focusing on increasing foreign exchange reserves, stabilizing inflation rates, and boosting arms production.

This new strategy gives these powers more maneuverability on the potential battlefield, a battlefield that seems to have been planned for years and is entering its final phase. The importance of this issue becomes even more apparent when we realize that despite the high military power of the United States and Britain, the debt-to-GDP ratio in these countries remains at critical levels. This reduces the economic support capacity for a war of attrition in the long term and has created an imbalance in combat-economic power.

Increasing threats in gray areas and possible scenarios by the end of 2025

According to many international analysts and researchers, by 2025, the world will no longer be at peace, but rather in a state of armed deterrence on the verge of ignition. Analysis of composite indicators shows that at least three global powers and two regional powers have reached a level of operational readiness close to the conflict phase.

If war breaks out in any of the sensitive areas, the likelihood of the conflict escalating to a multipolar level with the involvement of proxy forces and intense economic confrontation is very high. Existing trends indicate that in 2025, three main axes have the greatest potential for transition from tension to military conflict:

West Asia with centers such as the Red Sea and the occupied territories

In West Asia, some analysts are talking about possibilities such as a conflict between the Zionist regime and the axis of resistance by the end of 2025.

Another important scenario in this regard focuses on the role of the United States, and the possibility that the United States will enter a phase of targeted participation through limited operations in the Persian Gulf or extensive intelligence support. Of course, the current US administration has repeatedly stated that it wants an end to all conflicts in the Middle East, and the economic interests of the Donald Trump administration, in the White House’s declared policies, are tied to securing the macro-economic plans of actors such as Saudi Arabia, Qatar, and the UAE.

The third scenario in this area would be an increase in Yemeni attacks on the Zionist regime, an escalation of cyber-attacks on energy infrastructure, and even disruption of the Strait of Hormuz.

NATO-Baltic-Russia Eastern Front

According to some estimates, on the NATO-Baltic Eastern Front, the likelihood of a conflict escalation or a severe cyber-attack on NATO infrastructure in the remaining months until the end of 2025 is medium to high. This likelihood seems to increase in the final months of the year if conflicts related to the Ukraine war continue.

Meanwhile, Russia could launch a series of provocative attacks on NATO borders, which could increase the US military presence in Europe and divert Washington’s attention from the Middle East, an option that Moscow may not like. However, if such an event were to occur, Europe would gradually move towards an orange or even red alert.

Taiwan Strait and South China Sea

In the Taiwan Strait and South China Sea, by the end of 2025, there is a strong possibility that China will cross the psychological threshold of provocation against Taiwan. This is likely to emerge through threatening maneuvers or cyber-operations. In the meantime, the US response will be one of transparent but limited support and the likelihood of direct conflict between the US and China is low, but an increase in regional geopolitical tension in this part of the world is quite possible.

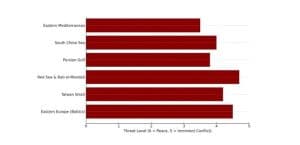

Chart explanation: The threat bar map shows the region’s most at risk of conflict by the end of 2025. The most dangerous regions are, in order: the Red Sea and Bab al-Mandab (4.7), the Baltic and NATO’s eastern borders (4.5), the Taiwan Strait (4.2), and the South China Sea and Persian Gulf (4.0 and 3.8) on a scale of 0 to 5.

In addition to the aforementioned scenarios, a hybrid scenario should not be neglected; a situation that could cause a significant shock to the global system. In this hybrid scenario, if conflict occurs simultaneously in the Middle East and the Baltics, several events will occur simultaneously:

– With the energy shock, oil will likely rise above $120.

– As these tensions intensify, we will see an increase in global inflationary pressure.

– Financial markets are crashing.

– Increased global cyber-activity and disruption of the global supply chain will be another likely event.